*Superior technology strategies with agile

digital management*

A contribution by Dr. Andreas Kipp and Dr. Alexander Fuchs (Short Version)

--- 06/01/2021

The technological, especially the digital throughput, will be the defining

and dominant element of this decade. This ultimately leads to a recognizable

and growing dominance of the technology sector. In all industries that are not

originally digital, a superior technology strategy - embedded in the overall

strategy for a sustainable unique business model - and its successful and

efficient implementation should be given top priority on the executive agenda, in particular of the CEO and CFO.

This leads to necessary rebalancing in the organization, with data and

digital sovereignty being integral. Companies need to use the strengths of

their industrial experience and invest in proprietary, agile digital solutions -

e.g. Cloud solutions, Information Technology versus

Operational Technology solutions (IT/OT) etc. - with a targeted use of

resources. In this way, every company and organization can maintain its own

unique identity with regard to the digital impact on its products, services and

operations (from Sourcing, R&D to Sales) under competitive aspects.

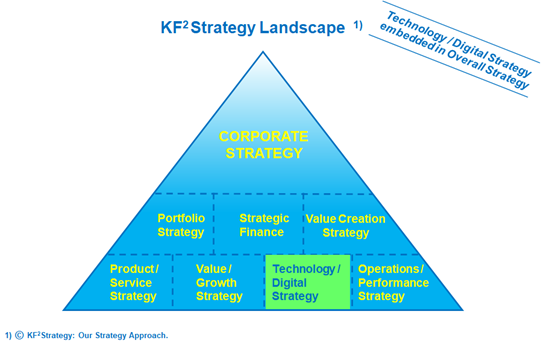

The strategy approach using the "KF2Strategy

Landscape" meets these requirements, taking into account the overall

strategic situation of the company.

The experience over the last years in discussion with the top management of

various industries shows that especially in Europe companies do rarely rely on

their own, valid and sustainable digital strategy, but rather loose valuable

time through indecisiveness and procrastination. The focus clearly needs to be

more content & implementation driven with less window dressing.

It is important to consider a concept which enables the best starting

conditions and growth options that are "in-line" with digital

governance & compliance. Many companies already have very good (partial)

concepts in use, but for the most part their integration and harmonization with

a competitive overall strategy and its successful implementation is pending.

Conflicting interests within the companies - e.g.

between functional areas like Sales/Marketing, R&D and Procurement - make

it challenging to balance individual needs and coordinate the best solutions. In

most cases, this overwhelms global players and medium-sized companies and poses

major challenges for ventures that are not originally digital tech companies.

It should be emphasized that even technology companies, hyperscalers

like Apple, Microsoft, Alphabet, AWS or SAP excluded, move into a

"niche", thereby frequently loosing sight

of the "big picture". Of course, this also makes their business model

vulnerable and creates attractive opportunities for non-original tech companies

in the competitive environment with regard to strategic considerations and

options for M&A, cooperations, etc.

.

The global M&A activities are at an "all time high",

especially in the area of technology. The dominance of M&A

investments in the technology industry and the dynamic growth of transactions

within the last 12 months are unparalleled (see also Refinitiv analysis). This

corresponds to the market capitalization of listed technology companies. The

dominance of the global technology industry in terms of market capitalization

and its average growth of well over 20% over the past 5 years leaves other

traditional industries, such as industrials, far behind (see also KF2Strategy

Global Macro Analysis 2020 /2021). The forecast 2021 of the relative global industry

market share of the global technology industry of over 5 trillion USD has joined

the market share leaders consumer staples and automobiles

and is growing steadily.

The relevance of the dynamically growing tech dominance is also reflected

in its rapidly increasing importance for institutional investors concerning

company appraisal and company valuation across all industries. Industries, like

mobility or financials are already particularly affected today. But what does

this mean for companies navigating in today’s competitive environment?

Non-original tech companies need to consistently develop their own

resources and competencies in order to create their own business identity and

business sovereignty for an agile sustainable business model with above-average

growth. In any case, this topic should be handled as a top priority throughout

the organization and get sufficient attention on every CEO agenda.